Women are the primary breadwinners in nearly half of U.S. households and they control half of the wealth in the United States. And with the upcoming generational wealth transfer, women are poised to control even more money and assets.

Recent research reveals that many women feel excluded from the financial services industry – to the detriment of women and banks alike. Only 26 percent of American women invest in the stock market (S&P Global). And only seven percent of the investing partners at the top 100 venture firms are women (Crunchbase).

Sallie Krawcheck, the CEO and founder of Ellevest and former CEO of Merrill Lynch’s wealth management division, said financial services firms are leaving at least $700 billion in revenue on the table each year by not meeting the needs of female customers.

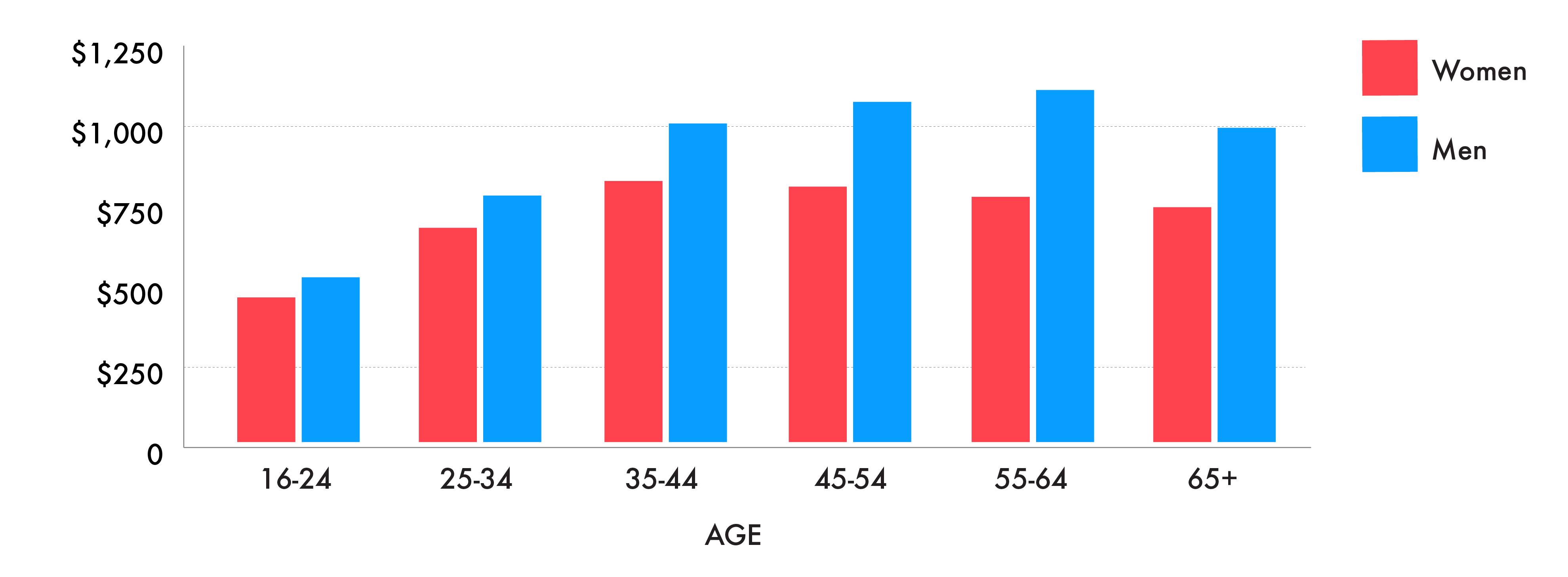

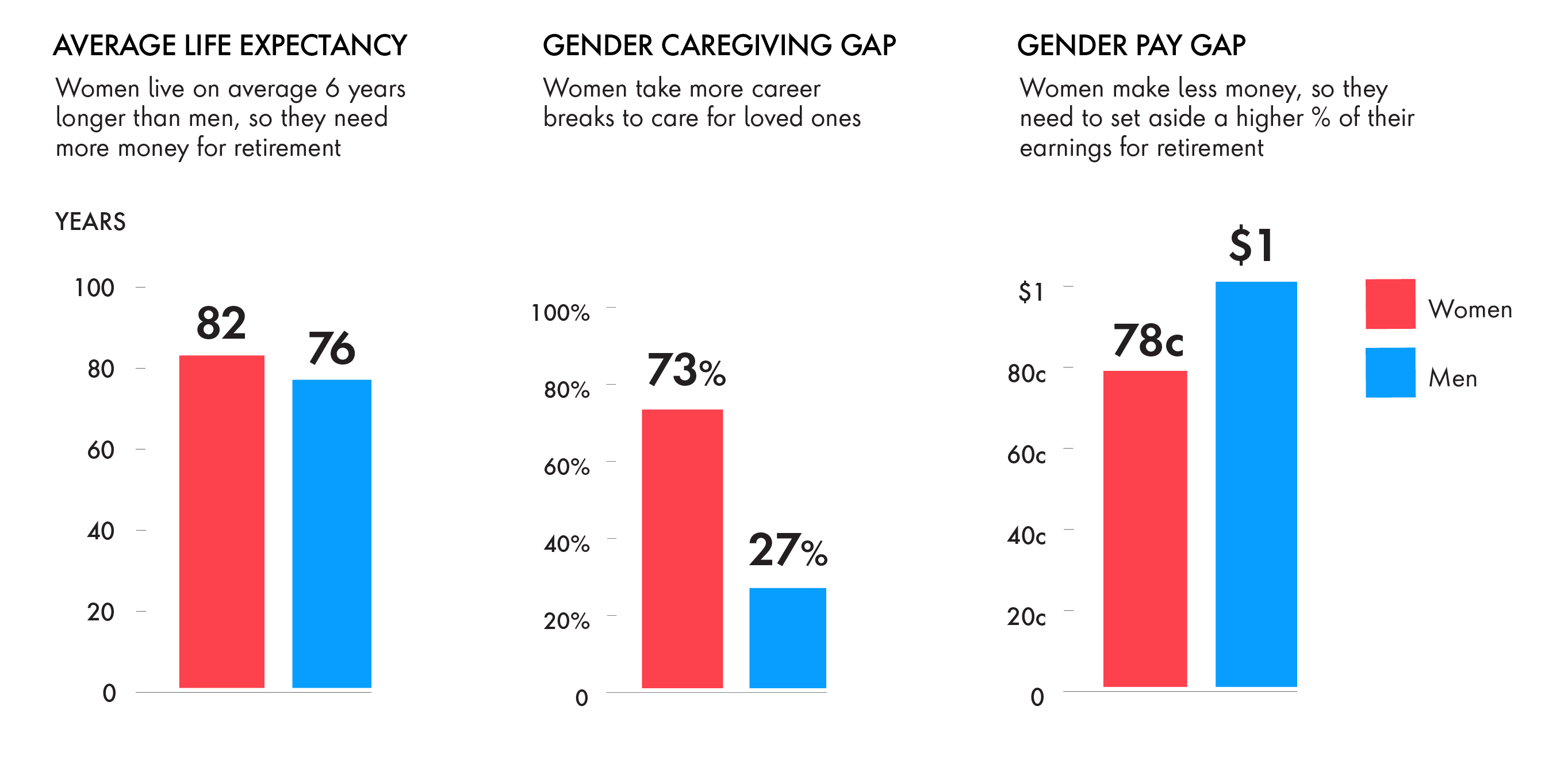

Money that’s not invested does not grow, and over a period of time, loses value due to inflation. On the other hand, men’s investments are growing. This contributes to women’s retirement account balances being a third lower than men’s overall (Prudential).

Lack of investments or retirement savings plus the gender pay gap create a phenomenon known as the wealth gap.

The wealth gap is a lose-lose situation – for women and for the wealth management industry. By helping to close the wealth gap, wealth managers and financial advisers will prosper with their female clients.

However, in order to serve women successfully, the financial industry needs to understand this problem’s underlying causes.

It starts early, and lasts a lifetime

GiftCards.com conducted a survey of 1,000 parents that found people were more likely to teach their daughters fiscal restraint and sons wealth building. Later in life, women were likely to tell Prudential researchers they didn’t have time to learn about financial products, industry jargon or investment management. Most didn’t even think they had enough money to invest.

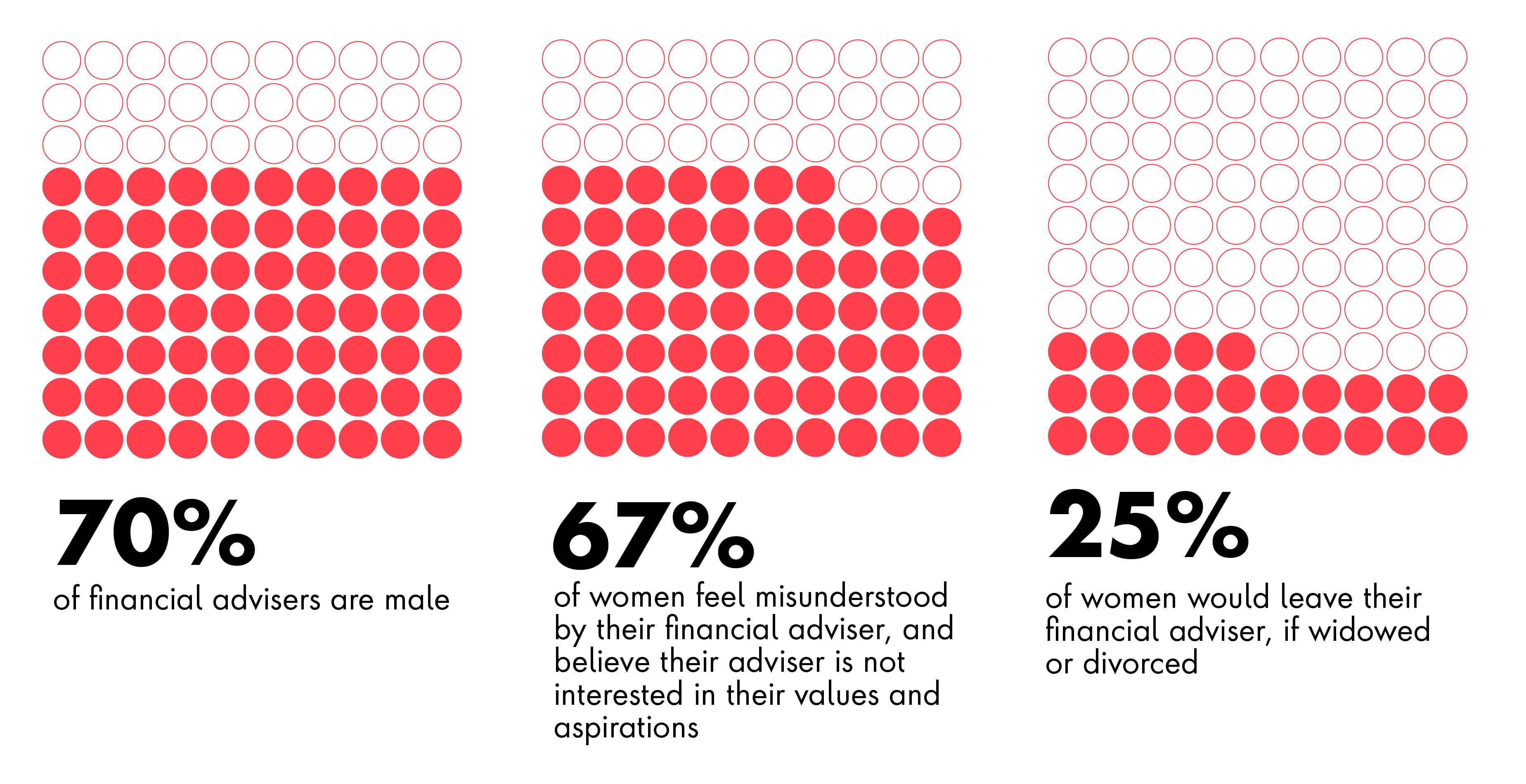

Seventy percent of financial advisers are male (Data USA). A survey by the Center for Talent Innovation found that sixty-seven percent of women feel misunderstood by their financial advisers, and believe they are not interested in their values or aspirations. A Prudential survey found that a quarter of women would leave their financial adviser if they were widowed or divorced.